AI, Credit 8 min read

AI agents in commercial credit underwriting: A responsible deployment guide

For many commercial credit teams, the challenge is familiar: how do you offer customers fast, competitive loan decisions while still maintaining the rigor that good underwriting decisions require?

It’s a difficult balance because commercial underwriting is rarely straightforward. Unlike consumer credit workflows, which can often rely on standardized inputs like credit scores or income limits, business applications require more interpretation. Financial statements tend to arrive in different formats, while important risk signals are often spread across multiple systems, sources, and files.

As a result, underwriters often spend valuable time preparing a case before they can properly assess it: checking whether an application is complete, normalizing financial data, and drafting credit memos. Each step matters, but together they can slow decisions, increase cost per application, and create unnecessary friction for customers.

This is where agentic AI can start to help.

AI agents are systems that can reason over a goal, interpret results, and determine next steps—including when to involve a human. In underwriting, agents are well suited to the parts of the process that require gathering context, processing messy documents and data, and drafting a summary for review.

For commercial credit teams, AI agents open up a practical path to making faster, more intelligent underwriting decisions. Not by removing human judgment, but by giving underwriters cleaner inputs, richer context, and more time to focus on the decisions that need their expertise.

Where AI agents can help in commercial credit underwriting

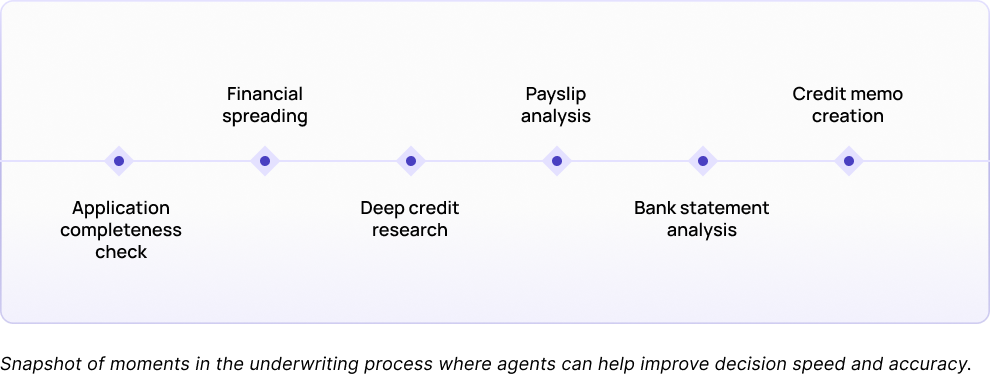

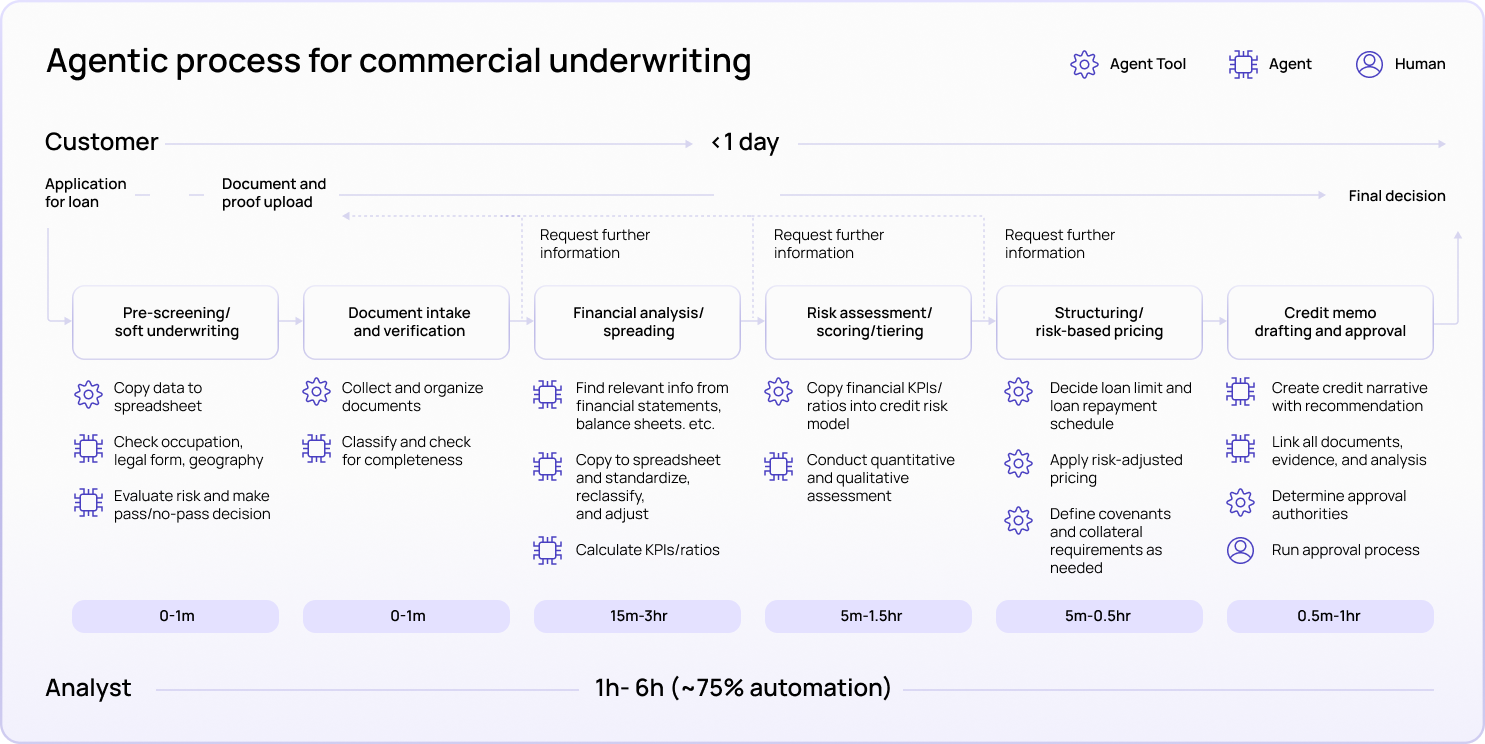

Taktile’s guide identifies four areas where credit teams can expand automation with agentic AI: document intake and application completeness checks, financial spreading and analysis, case management and human review, and credit memo creation.

Each of these areas has a common pattern: underwriters spend valuable time gathering, checking, and structuring information before they can make the actual credit decision. Agents can help by preparing the case, validating the inputs, and surfacing the right context for review.

Use case 1: Application completeness checks

One of the most immediate opportunities is application completeness.

Without agents, underwriters often need to manually review submitted documents to confirm whether all required information is present. When documents are missing or inconsistent, the customer may wait days before learning they need to provide additional information. That delay creates friction for the customer and interrupts the underwriting process.

With agents, completeness checks can happen before the application reaches the underwriter’s queue. An agent can review submitted documents, identify missing or inconsistent information, and prompt the customer to provide additional supporting material. Using OCR and natural language processing, the agent can also check whether the information in the documents aligns with public records or third-party sources.

Whether it’s a risk, product, or operational team, the value is clear: underwriters receive cleaner files, customers receive faster feedback, and the underwriting process becomes less dependent on manual back-and-forth.

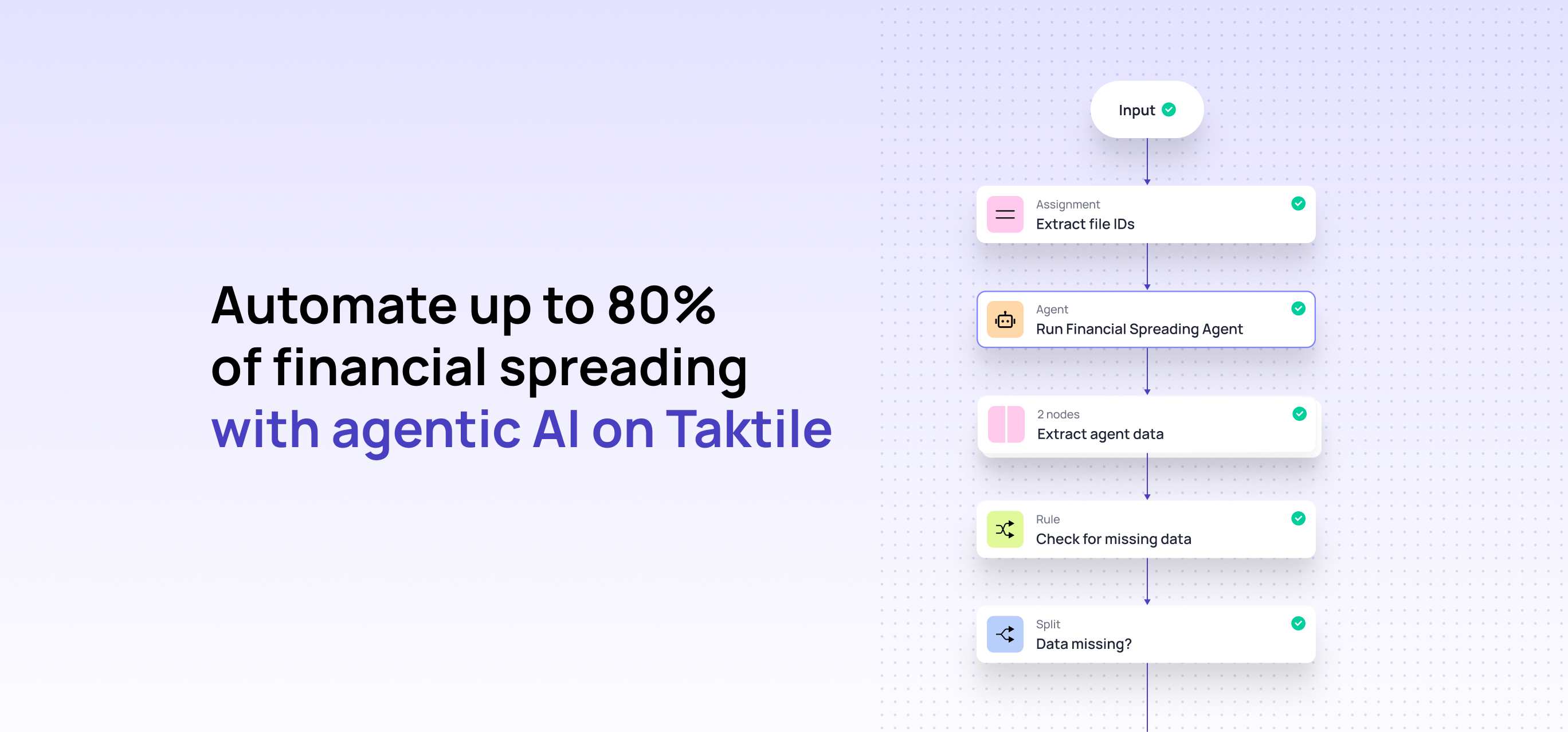

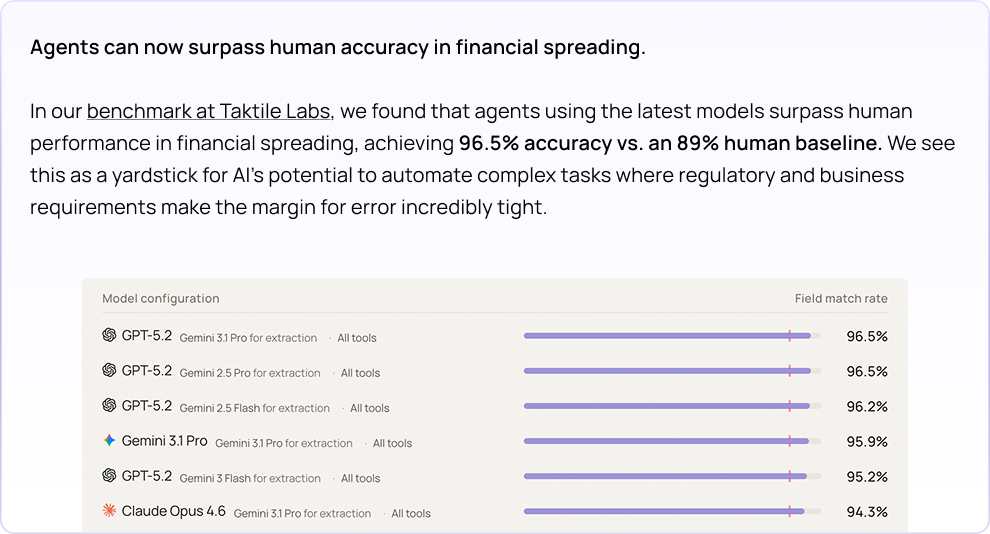

Use case 2: Financial spreading and analysis

Financial spreading is another high-impact area for agentic AI.

In commercial underwriting, financial spreading involves extracting data from income statements and balance sheets, normalizing that data into a standard format, and calculating the ratios needed for analysis. Because businesses present financial information in different formats, this work has traditionally required significant manual input.

Agents can digest financial statements, extract relevant data points, normalize them, validate figures, and flag discrepancies for review. For example, an agent can check whether line items add up correctly before the data is used in a credit model or credit memo.

For sophisticated institutions, this does not mean removing underwriters from the process. It means reducing the manual preparation work that delays analysis, while giving underwriters a more reliable starting point for decision-making.

Use case 3: Case management and human review

Even as teams begin using agents to automate more straightforward parts of the underwriting journey, human oversight remains essential for complex or higher-risk cases.

This is where agents can help make the review process more focused and informed. When an application sits close to a risk threshold, involves unusual financial patterns, or requires policy interpretation, an agent can surface the case to a human underwriter with the relevant context already attached.

Instead of asking reviewers to reconstruct the case from multiple documents, spreadsheets, and systems, agents can present the key inputs, risk signals, supporting evidence, and recommend the next step in one place. The underwriter remains responsible for judgment, but they can make that judgment with a clearer view of the full case.

For commercial credit teams, this creates a more practical model for human-agent collaboration: agents prepare and route the work, while underwriters focus their expertise on the decisions that genuinely require it.

Use case 4: Credit memo creation

As applications move toward final approval, agents can also support one of the most time-consuming parts of the underwriting process: preparing the credit memo.

A credit memo brings together the information collected throughout the application journey, including customer details, financial analysis, relevant ratios, risk signals, policy considerations, and supporting evidence. Creating that narrative manually can take significant time, especially when information is spread across documents, spreadsheets, and internal systems.

With agents, teams can generate a draft credit memo based on the information already gathered and analyzed during the underwriting workflow. Reviewers can then refine the memo, inspect the underlying evidence, and make the final decision with a clearer view of how the recommendation was formed.

The goal is not to remove review from the process. It is to give approvers a more complete, consistent starting point: one that links the credit narrative back to the data, documents, and analysis behind it.

What responsible deployment looks like

For commercial credit teams, deploying agents responsibly starts with an important shift in thinking: the goal is not simply to prove that a model can perform a task well. The goal is to understand how agents can operate safely and reliably within the underwriting process around them.

That means looking beyond the agent itself and designing the right system of context, controls, human review, and monitoring.

Context layer: Agents need access to the same information a strong underwriter would use, including customer documents, internal data, third-party sources, historical decisions, and relevant policy context.

Deterministic layer: Fixed credit policies, eligibility rules, and non-negotiable thresholds should remain governed by rules. Agents are most useful for work that requires interpretation, investigation, or multi-step reasoning.

Human review layer: Higher-risk, unusual, or borderline applications should be routed to reviewers with the agent’s recommendation, supporting evidence, reasoning, and areas of uncertainty clearly visible.

Monitoring layer: Every agent action should be traceable, including the data accessed, tools called, recommendation made, and final human decision. This supports auditability while helping teams improve performance over time.

Together, these layers help commercial credit teams move from experimenting with standalone agents to building agentic underwriting workflows that are governed, explainable, and ready to scale.

How to get started

For commercial credit teams exploring agentic AI, a helpful first step is to start with the workflow challenge rather than the agent itself.

Instead of asking, “Which agent should we build?”, it can be more useful to ask: “Where is manual work creating the most friction in our underwriting process today?”

For some teams, that friction may show up during application completeness checks. For others, it may be financial spreading, credit memo creation, or escalated case review. The best starting point is usually a workflow that is narrow enough to test safely, meaningful enough to improve the underwriting experience, and measurable enough to show whether the agent is creating value.

A few useful metrics to consider include:

- Time from application submission to first decision

- Cost per underwriting decision

- Share of applications requiring manual document follow-up

- Financial spreading accuracy

- Human override rates

- Customer drop-off during the application process

- Reviewer satisfaction and time saved

The goal is not to automate commercial underwriting all at once. A more practical path is to identify the moments where agents can help prepare cleaner cases, reduce repetitive manual work, and give underwriters more time and context for the decisions that need their expertise.

As commercial credit teams begin exploring agentic AI, the most valuable opportunities will come from workflows where speed, consistency, and human judgment all matter.

If you’re exploring where AI agents could support your own underwriting workflows, download the full guide for a practical framework to evaluate opportunities, design guardrails, and scale responsibly across credit underwriting, as well as AML, compliance, and fraud use cases.

Frequently Asked Questions (FAQ)

What is an AI agent in commercial credit underwriting?

An AI agent in commercial credit underwriting is a system that can reason over an underwriting goal, use tools and data sources, interpret unstructured documents, and determine next steps such as validating an application, extracting financial data, drafting a credit memo, or escalating a case for human review.

Where can AI agents create the most value in commercial underwriting?

High-impact areas include application completeness checks, financial spreading, case preparation, human review workflows, and credit memo creation.

Should AI agents make commercial credit decisions autonomously?

Not always. Lower-risk or straightforward cases may be candidates for greater automation over time, but complex cases should be routed to human reviewers with full context, evidence, and agent reasoning available.

What guardrails are needed for AI agents in credit underwriting?

Institutions need clear data access controls, fixed policy rules, escalation thresholds, human review workflows, audit trails, and performance monitoring.